This week the IRS issued additional guidance on Families First Act

Click here for an updated overview of the law and up-to-date FAQ’s.

March 19, 2020 (Original Memo Date)

Revised March 25, 2020 (Revisions/Additions from Original Memo are in RED)

For all further updates please click the Frequently Asked Questions information below.

FAQ’s March 27, 2020

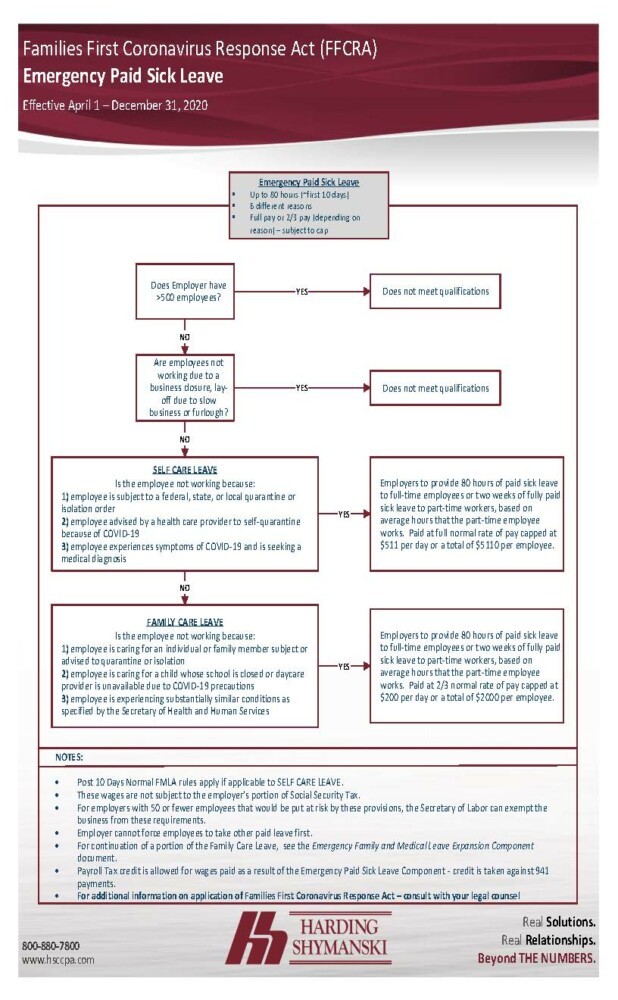

Click here for some helpful flowcharts regarding Families First Coronavirus Response Act.

Families First Coronavirus Response Act – Guidance Related to Required Paid Sick Leave, Extended FMLA Requirements and Payroll Tax Credits Designed to Fund These Required Payments

Introduction

Please note that the items discussed in this memo should be discussed with legal counsel. We are attempting to provide a summary of the rules based on our understanding of them but we are not a law firm and we cannot provide legal advice.

Also, please note that the Department of Labor, at the time of this writing, has issued limited guidance on this act and we have incorporated that guidance into this memo. Additional guidance from the DOL will be critical in fully understanding the act in more detail.

The provisions discussed below become effective April 1, 2020 and extend through the end of 2020. These rules apply to employers with fewer than 500 employees. This is not retroactive and the paid leave and payroll tax credits discussed in this memo cannot be taken until April 1, 2020. April 1st is a new date that was clarified by the DOL. It is also our current understanding that this act and the related credits are only available for paid leave for time paid starting April 1st or after and is not based on the pay date but is based on the date the time was taken off and paid. The check date does not appear to be the relevant date to focus on but the date that the leave is taken and paid for under this act. Example: If someone is off on March 29th March 30th and March 31st and the employer chooses to pay them for that time and that payroll is paid on April 2nd, that time from March 29th through March 31st is not eligible for this act and no payroll credits would be applied to it and those amounts paid would be taxed like normal paid leave.

Based on current materials available, we have created this guidance to help you understand these rules. This may be modified at a future time as more information becomes available. The Families First Coronavirus Response Act recently signed into law by President Trump is designed to do two primary things:

- Provide a safety-net for employees of companies with fewer than 500 employees who cannot work due to Coronavirus related situations. The Department of Labor is using language pointing to FLSA and regular FMLA rules for determining which employers need to be aggregated for purposes of this determination. We recommend consulting a labor attorney for assistance with this determination if there is any question. Please note that this determination is not based on tax code controlled group rules and the rules for aggregating employers for this purpose is different so please consider that.

- Please note that this act does NOT require employers to pay employees if they are not working due to a business closure, lay-offs due to slow business or furloughs.

- Provide employers a mechanism to be reimbursed via payroll tax credits to be claimed by reducing otherwise due and payable federal payroll and federal withheld income taxes as you submit them each pay cycle. This is the mechanism you will use to fund these new required payments to employees. An employer does not have to wait until they file their quarterly Form 941 to claim the credit but instead, it is immediately available as a reduction in otherwise payable taxes.

Safety Net for Employees Portion of Law

This summary will first focus on item one above. This act addresses providing a safety net to employees in two primary ways. They are the “Emergency Paid Sick Leave” component and the “Emergency Family and Medical Leave Expansion” component of the act, each to be discussed now.

Emergency Paid Sick Leave Component

This provision provides for up to 2 weeks of fully paid leave for the reasons discussed below for any employee of the company, and there is no waiting period to be eligible for this portion of the law. This portion of the act requires employers to provide:

- 80 hours of fully paid sick leave to full-time employees or

- Two weeks of fully paid sick leave to part-time employees, based on the average hours that the part-time employee works.

This paid leave requirement would be triggered if an employee were unable to work for one of six reasons:

- To self-isolate due to federal, state or local requirements. There are some unknowns in this category as to what rises to this level. If a governor of a state issues an order to close certain businesses, do the employees of that business fall into this category at that time? We need additional guidance on this and this is a common question that is being asked.

- To quarantine due to COVID-19 concerns on the advice of a health care provider.

- To obtain medical diagnosis or medical care if the employee has COVID-19 symptoms.

- Please note these first three categories are referred to as “Self-Care Leave” to be discussed further below.

- To care for someone (very broad definition, such as Parent, Spouse, Child, Sibling, Next of Kin, Grandparent, Grandchild, Senior Citizen, Individual with Disabilities) experiencing one of the first two situations listed above.

- To care for the employee’s son or daughter (under age 18) if the school or daycare provider has closed or if the daycare provider is no longer available due to COVID-19.

- The employee is experiencing another substantially similar condition to those above.

- Please note these last three categories are referred to as “Family Care Leave” to be discussed next.

Leave in the first three categories, called “Self-Care Leave,” has to be paid at the employee’s full normal rate of pay but that is capped at $511 per day or $5,110 total for each employee. Leave in the last three categories, called “Family Care Leave,” has to be paid at 2/3’s of their normal rate of pay but that is capped at $200 per day or $2,000 total for each employee. It is important to note that an employer CANNOT require an employee to use any existing paid leave provided by an employer before using this newly required paid leave.

The DOL can exclude certain healthcare workers and emergency responders from having to comply with this act. At this time, the definition of what qualifies as a healthcare worker is not clear. Based on what we have read, the entire company that is a health care provider is not exempt from this act, only the employees that work for that employer as a health care provider are exempt. Support employees not in the field of providing health care are required to be covered by this act.

The DOL MAY also exempt small businesses from portions of this act with fewer than 50 employees if complying would put the business in jeopardy. At this time, the DOL has said they will be issuing more guidance on this under 50 employee exemption but in general it only applies if following this acts rules would jeopardize the viability of the business.

PAYROLL TIP: It is important to note that from a payroll logistics standpoint, new and separate earnings codes will need to be set up in the payroll system to be able to track each of these newly required types of payments. That will be critical to effectively quantify the dollars paid for these types of leave and will make it possible to claim the payroll tax credit to be discussed later in this article. Do not lump this pay in with any other PTO or sick leave payments that you might otherwise make.

Emergency Family and Medical Leave Expansion Component

This provision requires employers (even those with less than 50 employees who are not normally subject to normal FMLA rules) to protect an employee’s job and pay compensation after the first two-week period has lapsed as discussed below.

This new category of leave under FMLA rules is referred to as “Public Health Emergency Leave” and requires employers to pay employees who are unable to work due to a need to care for a child under age 18 if school or daycare is unavailable due to Covid-19. Under this rule, employers are required to:

- Provide “Public Health Emergency Leave” as part of FMLA leave.

- Provide “Public Health Emergency Leave” if needed by ANY employee who has been employed for at least 30 calendar days.

- Pay eligible employees at a leave rate of NO LESS than 2/3’s of their normal rate of pay. This kicks in after 10 days have passed. Please note that this portion of the law is intended to run concurrent with the emergency paid sick leave component just discussed. If an employee qualifies for this portion of the act based on the same event that qualified them for the emergency paid sick leave pay, this portion is an additional 10 weeks. The total would be 12 weeks of protected leave and 12 weeks of pay. This pay is capped at $200 per day and $10,000 in total per each employee.

The DOL can exclude certain healthcare workers and emergency responders from having to comply with this act. At this time, the definition of what qualifies as a healthcare worker is not clear. Based on what we have read, the entire company that is a health care provider is not exempt from this act, only the employees that work for that employer as a health care provider are exempt. Support employees not in the field of providing health care are required to be covered by this act.

The DOL MAY also exempt small businesses from portions of this act with fewer than 50 employees if complying would put the business in jeopardy. At this time, the DOL has said they will be issuing more guidance on this under 50 employee exemption but in general it only applies if following this acts rules would jeopardize the viability of the business. Employers with fewer than 25 employees do not have to comply with the job protection aspect of this bill, but do have to provide the pay.

It is important to note that this provision is in addition to all normal FMLA rules that already exist for employers that must comply with the existing FMLA rules.

PAYROLL TIP: It is important to note that from a payroll logistics standpoint, new and separate earnings codes will need to be set up in the payroll system to be able to track each of these newly required types of payments. That will be critical to effectively quantify the dollars paid for these types of leave and will make it possible to claim the payroll tax credit to be discussed later in this article. Do not lump this pay in with any other PTO or sick leave payments that you might otherwise make.

Funding Mechanism Available to Employers to Pay These New Wages

Now that we have addressed the safety-net components set in place to protect employees, let us turn our attention to the second component of this act, which is the mechanism put in place to fund these payments for the employer.

Any wages paid as a result of the provisions discussed above are not subject to the Employer portion of Social Security Tax (the 6.2% payroll tax). They are subject to the Employee portion of this tax, however – that must be withheld from the payments made to the employee. Because these wages are not taxed the same as normal sick pay or PTO pay, you must segregate these wages in your payroll system.

In addition to these new wages not being subject to the employer portion of Social Security tax as they are paid, this law also provides a refundable credit to be applied to reduce otherwise due and payable federal social security, Medicare and federal income tax withholdings on normal wages paid each pay period. In essence, a credit is given to the employer that allows them not to have to pay otherwise required payroll taxes and that is the mechanism to quickly reimburse the employer for having to pay wages under this act. If the amount of the credit is more than otherwise due and payable taxes for a pay period, there is going to be a process (not yet defined) to allow the employer to get a refund check mailed to them within 2 weeks of that submission. Also, the process to claim the credit at the time of submitting otherwise due and payable payroll taxes is not yet defined. Finally, there is a component to this credit also for health insurance costs paid on behalf of an employee on leave under this act as well. We need additional guidance on that at this time. As we mentioned earlier in our PAYROLL TIP sections, this is why it is important for employer to be able to separately identify compensation paid to employees as a result of this act. The amount of the credits available are as follows:

- For the wages paid as a result of the “Emergency Paid Sick Leave Component” (first two weeks) of the act, the credit is equal to the amount of the wages paid required by this act.

- For the wages paid as result of the “Emergency Family and Medical Leave Expansion Component” (after first two weeks) of the act, the credit is equal to the amount of wages paid required by this act and is capped at $10,000 per employee.

- In the aggregate, the sum of the credits available in number 1 and 2 can be as much as $15,100 per employee. (Up to $5,100 in wages for the first two weeks + $10,000 for the FMLA portion). Given that the employer’s share of social security tax on any individual employee is limited to $8,537.40 ($137,700*6.2%), this credit is meaningful and actually can exceed the actual social security tax paid for an individual.

- As mentioned earlier, there is also a component of this credit that is tied to the amount of health insurance paid by the employer on behalf of an employee out on leave under this act. At this time, we need more clarification on this part of the credit. One unknown is does it go above and beyond the caps discussed in number 3 above or is that cap inclusive of this portion for the credit?

We feel it is important that employers that may be potentially impacted by these new rules work now with their payroll systems to create the earnings codes necessary to track and tax these new types of wages correctly.

Click here for a PDF version of this article.

Please reach out to Matt Folz 812-491-1391 or Lisa Frank 812-491-1312 at Harding, Shymanski & Company, P.S.C. for further discussions related to this matter